Auto Loan Calculator

Calculate payments over the life of your Loan

Home Blog Privacy Terms About ContactCalculate payments over the life of your Loan

Home Blog Privacy Terms About ContactPublished on October 12, 2025

This is a personal story about my own loan experience and the mistakes I made. It is not financial advice. Please consult a qualified professional for your financial decisions.

The fluorescent lights of my office cubicle seemed to hum with a special kind of monotony. For two years, I had been stuck in a job that wasn't just a dead end; it was a maze with no cheese at the end. I felt my skills stagnating, and a quiet panic had started to bubble up inside me. I knew I needed a change—a big one.

That's when I discovered it: an intensive, career-changing coding bootcamp. It felt like a lifeline. The program promised in-demand skills and a path to a career I could actually be excited about. The only catch? The tuition was a steep $14,000. I didn't have that kind of money just sitting around, so a personal loan seemed like the only logical next step.

My emotional state was a mix of intense hope and overwhelming urgency. This bootcamp was my ticket out, and I didn't want to miss the upcoming session. In my mind, the loan was just a simple administrative hurdle. I assumed the process would be straightforward: apply, get approved, pay the tuition, and start my new life. I banked with the same institution I'd used since I was a teenager, a place where I felt a sense of familiarity and, I thought, loyalty.

Just as I started researching, an email landed in my inbox from my bank. "You're Pre-Approved!" it shouted in a friendly blue font. It felt like a sign. The offer was for up to $15,000, and it seemed so easy. I figured, "They know me, they have my accounts, this must be the best deal I'm going to get." That single, comfortable assumption was the start of a mistake that would cost me dearly, a mistake I wouldn't even realize I'd made until months later.

The application process with my bank was exactly as smooth as I had hoped. I filled out the form online in about ten minutes, leveraging the "pre-approved" status they had offered. Within 24 hours, the final offer was in my portal: a $14,000 loan with a 48-month term and a 13.99% APR. The monthly payment came out to about $381. It felt manageable, and more importantly, it was done. I clicked "accept" with a huge sigh of relief, paid the bootcamp tuition, and dove headfirst into my new career path.

For three months, I was completely absorbed in learning to code. I barely thought about the loan, other than making the automatic monthly payments. The stress of my old job was gone, replaced by the satisfying challenge of learning something new. I felt like I had made the best decision of my life. Then, a random Tuesday afternoon changed my perspective.

I was sifting through a pile of mail—mostly junk—when I saw a letter from a different, online-only lender. It was another one of those pre-qualified offers, and I almost tossed it directly into the recycling bin. But for some reason, I paused. The interest rate advertised on the front in bold print seemed significantly lower than what I was paying. Curiosity got the better of me. "There's no way it's that simple," I thought, but I opened my laptop anyway.

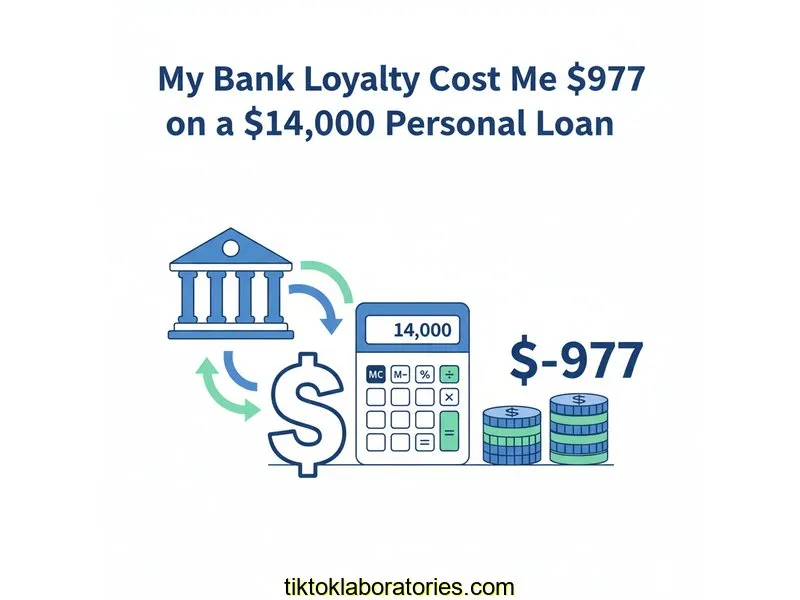

I navigated to an online loan calculator and plugged in my original loan amount, $14,000, and the 48-month term. First, I entered my current 13.99% APR. The calculator showed a total interest cost of over $4,200. Then, with a feeling of detached curiosity, I entered the 10.99% APR from the mailer. The screen refreshed, and my stomach dropped. The total interest cost was just over $3,300. The difference was a staggering $977.

It wasn't a hypothetical number. It was real money I was committed to paying, simply because I didn't look anywhere else. I re-ran the calculation three times, thinking I must have made a mistake. But the numbers were correct. My loyalty to my bank, my desire for a quick and easy process, had a clear price tag: almost one thousand dollars. I felt a wave of frustration wash over me, not at the bank, but at myself. In my haste to secure my future, I had completely overlooked the present financial reality.

To truly understand where I went wrong, I had to be brutally honest with myself. My approach was driven by emotion and convenience, not by financial diligence. Seeing the numbers laid out in black and white was the only way for me to process the full extent of my oversight. I created a mental table to compare the path I took with the one I should have taken. It was a painful but necessary exercise.

Playing this out in my head, I realized a few simple steps could have saved me a lot of money and regret. This isn't advice, but a blueprint of what I will do next time, based on this hard lesson.

My first action should have been to acknowledge the emotional pressure I was under. The urgency I felt was real, but it was clouding my judgment. I would have told myself that an extra week of research to save nearly a thousand dollars was a worthwhile investment of time.

Before even looking at lenders, I would have pulled my own credit reports and scores. This would have given me a baseline understanding of what kind of rates I could realistically expect, making me a more informed shopper from the very beginning.

Instead of stopping at my bank, I would have used their offer as a starting point. I would have spent one afternoon applying for pre-qualification (which typically uses a soft credit check) with a major credit union and two or three highly-rated online lenders. This would have given me a handful of real offers to compare side-by-side.

With those offers in hand, I would have put them into a basic spreadsheet. The columns would have been: Lender Name, Loan Amount, APR, Term (in months), Monthly Payment, Origination Fee, and Total Interest Paid. Seeing the numbers in a grid like that would have made the best option immediately obvious.

Armed with clear data, I could have confidently chosen the loan with the lowest total cost, not the one that felt easiest or most familiar. My loyalty would have been to my own financial well-being, not to a banking brand.

This experience, while frustrating, was an incredibly valuable teacher. It fundamentally changed how I view major financial decisions. I boiled down my reflections into a few key principles that I will carry with me from now on.

In the months since this discovery, I've spent a lot of time reflecting. It's easy to just be angry, but I found it more productive to ask myself some tough questions to make sure I don't repeat the same mistake. This was my experience, and yours may be completely different, but these are the questions that helped me process what happened.

In my case, the answer was a combination of fear and excitement. I was afraid of being stuck in my old job and excited about the new opportunity. This emotional cocktail made me prioritize speed over diligence. I let the bootcamp's start date create a false sense of urgency for the financing part of the plan.

Honestly, it never even crossed my mind. I saw the pre-approved offer as a take-it-or-leave-it deal. I didn't realize that in some cases, there might be room for negotiation, or that they might be willing to match a competitor's offer. I never gave myself the chance to find out because I didn't do the research to get a competing offer in the first place.

It's interesting to me that I ignored countless online ads but paid attention to a piece of physical mail. For me, I think holding it in my hand made it feel more real. It was a tangible prompt that forced me to stop and think, breaking through the digital noise and my own focused bubble. It was a random, lucky trigger for a very important lesson.

Yes, absolutely. Despite the extra cost, the loan enabled me to change my career, which has been immensely rewarding both personally and financially. I don't regret taking out a loan. What I regret is the way I took it out. This helps me separate the outcome from the process and focus on improving the process for the future.

The single most important lesson I will carry with me from this entire experience is this: I have to be my own financial advocate. No bank or lender has my best interests at heart more than I do. Their goal is to make a profit, and my goal is to secure the funds I need at the lowest possible cost. Those two goals are not always aligned.

It can feel intimidating to navigate the world of loans, especially when you're under pressure. My story shows that even a small oversight, born from a desire for simplicity, can have a real financial impact. But it also shows that it's never too late to learn. I'm now paying off that loan every month with a new sense of awareness.

Every payment is a reminder to slow down, to do the research, and to always, always compare my options. It's a $977 lesson, and I plan on getting my money's worth. Thank you for letting me share my story.

Remember, this is just my personal story and the financial path I walked. Always consult with a qualified financial advisor for your specific situation.

Disclaimer: This article documents my personal experience with a loan. This is not financial advice. Your own situation, creditworthiness, and loan options will differ. I am not a financial professional. Always consult with a qualified financial advisor, review all loan documents carefully, and compare multiple lenders before making any financial decisions. Loan terms, rates, and fees vary widely.

About the Author: Written by Alex, someone who has navigated the world of personal finance for over 8 years, making plenty of mistakes and learning from them along the way. I'm not a financial advisor or loan officer—just an individual sharing personal stories to help others feel less alone in their financial journey. My experiences are my own; always seek professional guidance for your specific needs.